Traditional credit scores are no longer enough. In an era where millions transact daily through UPI but remain invisible to credit bureaus, banks need a smarter, real-time credit evaluation model designed for digital ecosystems.

That’s where UPI-based behavioural credit scoring and UPI-based lending come in—using live transaction data to assess risk, unlock lending, and drive financial inclusion.

In this blog, we’ll explore how banks can cut defaults, grow approvals, and tap into untapped segments—all through the power of CARD91’s AI-powered credit engine for UPI credit scoring.

The Problem with Legacy Credit Models

Traditional credit evaluation has failed to evolve with the digital consumer. Here’s why legacy credit models are struggling in today’s digital lending environment:

1. Static, Outdated Bureau Data

Credit bureaus update their records infrequently, which means lenders may be assessing applicants based on months-old data. This creates a blind spot in fast-paced, real-time credit evaluation in India.

2. Exclusion of New-to-Credit Customers

India has millions of digitally active users—especially in the gig economy—who lack formal credit histories. Legacy models simply filter them out, limiting financial inclusion and stalling UPI-based lending.

3. High Defaults Due to Poor Risk Segmentation

Without behavioural insights, lenders often group diverse borrowers into the same risk category. This leads to poor underwriting, higher NPAs, and misaligned credit limits.

Enter: AI-Powered UPI Credit Scoring

What Is It?

UPI-based credit scoring uses AI and machine learning to analyze real-time UPI transaction data. It looks at payment behaviour—frequency, patterns, peer-to-peer transfers, bill payments, and more—to build a dynamic behavioural credit score.

Why UPI Data Matters

UPI activity reflects how individuals manage day-to-day finances in real time. It’s dynamic, data-rich, and more indicative of actual repayment capacity than static credit bureau scores—perfect for digital lending using UPI data.

Real-Time vs Traditional Scoring

Unlike bureau scores that update monthly or quarterly, UPI-based behavioural scores adapt daily—enabling banks to operate with real-time credit evaluation in India for smarter decision-making.

Key Benefits for Banks

1. Lower NPAs Through Early Risk Detection

Catch risk signals early through spending anomalies, sudden inactivity, or irregular payment patterns. This helps mitigate delinquencies before they snowball—reducing losses in UPI-based lending portfolios.

2. Faster, Automated Underwriting

AI-driven insights eliminate manual dependencies. CARD91’s AI-powered credit engine ensures faster, consistent underwriting—ideal for digital lending using UPI data.

3. Higher Loan Approvals with Better Risk Control

By scoring and segmenting more accurately, banks can approve more loans while maintaining tight control on portfolio quality.

4. Inclusion of Underserved and NTC Segments

Reach thin-file, self-employed, and new-to-credit individuals confidently—backed by real-time behavioural insights.

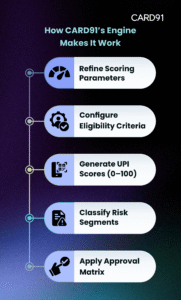

How CARD91’s Engine Makes It Work

CARD91’s UPI Credit Score Engine is built for precision, speed, and inclusion—making UPI-based lending a reality at scale. Here’s how the AI-powered credit engine functions:

Refine Scoring Parameters AI/ML models analyze historical UPI transaction data to identify the most relevant variables and weightages for creditworthiness.

Configure Eligibility Criteria Lenders can define eligibility based on income levels, transaction behaviour, and demographics to focus on the right customer base.

Generate UPI Scores (0–100) Each customer receives a behavioural score that updates in real time—essential for accurate, real-time credit evaluation in India.

Classify Risk Segments Borrowers are segmented into High, Medium, or Low risk groups—enabling personalized and precise decision-making.

Apply Approval Matrix Each segment is linked to defined rules—automated approvals, manual reviews, or rejections—ensuring consistency and compliance.

Real-World Use Cases

CARD91’s behavioural scoring engine is already driving success in real-world UPI-based lending environments:

SME Lending Many small businesses lack bureau scores. UPI transaction patterns help assess financial discipline and working capital needs.

Personal Loans Freelancers, gig workers, and thin-file individuals can now be confidently assessed using digital lending models powered by UPI data.

BNPL & Microcredit For micro-loans, real-time credit evaluation in India ensures borrowers are screened dynamically, improving repayment predictability.

Conclusion

In a world where UPI transactions are the new credit signals, traditional credit scores are falling behind.

CARD91’s AI-powered credit engine for UPI credit scoring brings precision, inclusion, and speed to modern digital lending workflows—helping you lower defaults, expand access, and lend confidently.

The future of lending is behavioural. Book a demo today and see how CARD91 is shaping the next era of UPI-based lending in India.