Unify signals from PAN, Aadhaar-linked checks, GST, phone attributes, vehicle data, court records, EPFO, and digital footprint in one verification flow.

Convert fragmented verification signals into a single confidence score with clear risk bands for faster triage and smarter decisioning.

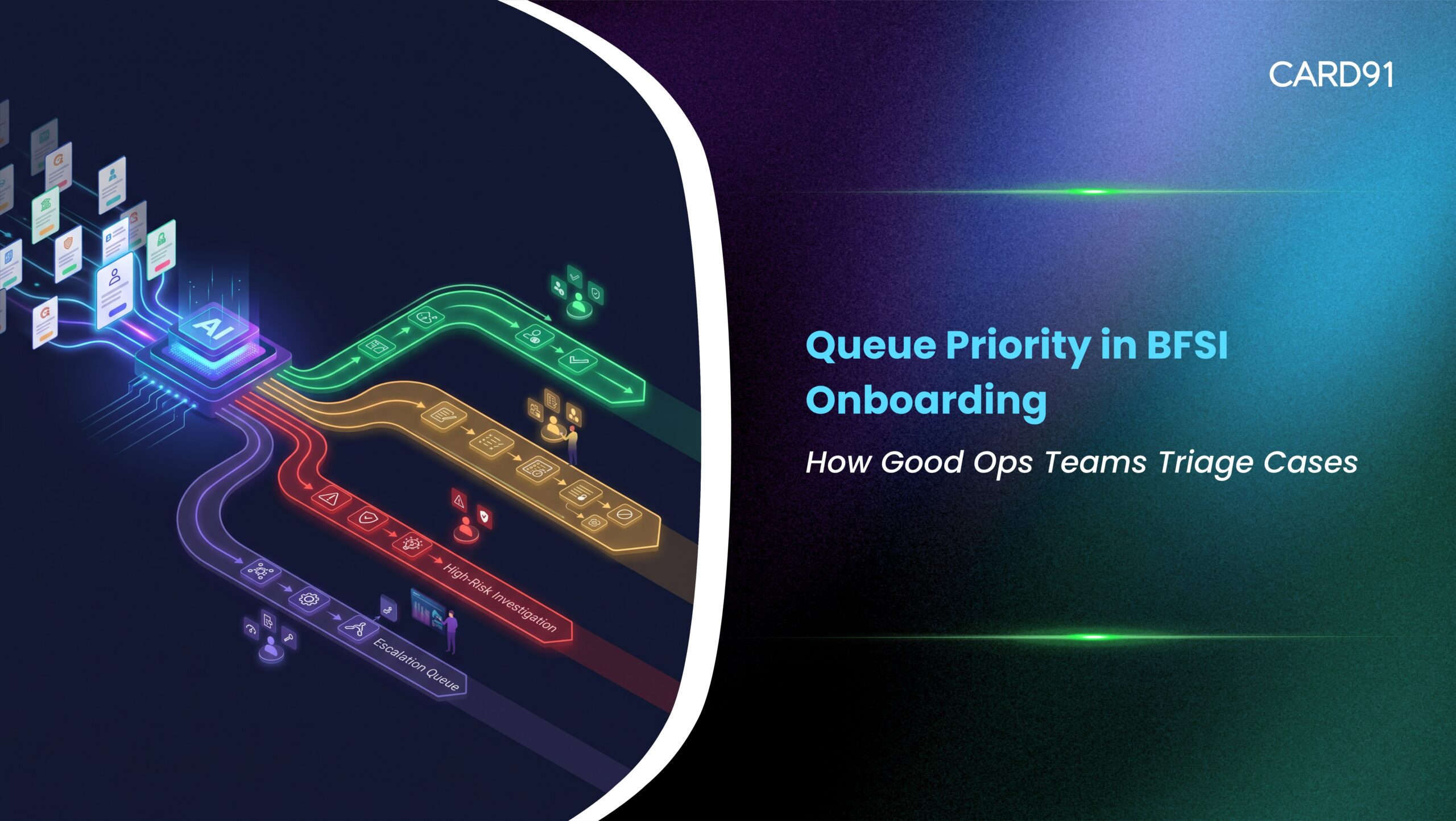

Route cases into approve, review, or reject workflows using real-time verification outcomes and configurable rules.

Set score bands, thresholds, parameter weights, and workflow logic based on your institution’s risk appetite, product type, and policy framework.

Go beyond basic verification with re-verification rules and additional fraud intelligence signals.

Unify signals from PAN, Aadhaar-linked checks, GST, phone attributes, vehicle data, court records, EPFO, and digital footprint in one verification flow.

Convert fragmented verification signals into a single confidence score with clear risk bands for faster triage and smarter decisioning.

Route cases into approve, review, or reject workflows using real-time verification outcomes and configurable rules.

Set score bands, thresholds, parameter weights, and workflow logic based on your institution’s risk appetite, product type, and policy framework.

Go beyond basic verification with re-verification rules and additional fraud intelligence signals.

Start modernising your payments with CARD91 infrastructure

To know more about our offerings connect with our experts