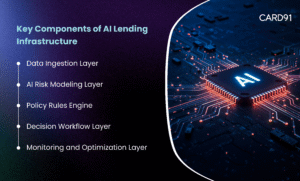

A modern AI lending infrastructure consists of several interconnected components that support intelligent credit decisioning.

This layer collects borrower information from multiple sources such as:

The purpose of this layer is to standardize data so it can be used effectively by risk models and decision engines.

Machine learning models analyze borrower data to estimate credit risk.

These models can identify complex relationships between financial behavior, transaction patterns, and repayment probability.

The AI risk model generates risk scores that support underwriting decisions.

While AI models provide risk predictions, lenders still require policy control.

Rules engines allow financial institutions to define:

This ensures automated decisions remain aligned with lending policies.

Not all loan applications should be automatically approved or declined.

Decision workflows allow lenders to route applications based on risk signals.

Examples include:

Workflow orchestration ensures underwriting decisions are executed consistently.

Effective AI credit decisioning requires continuous monitoring.

Lenders must track metrics such as:

Continuous monitoring allows lenders to refine underwriting strategies and improve portfolio quality.