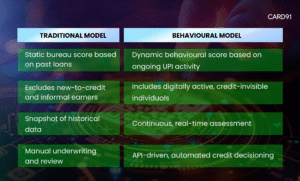

This transformation doesn’t replace traditional bureaus—it enhances them. By layering behavioural intelligence over existing credit data, lenders achieve a 360-degree risk view, blending historical reliability with current intent.

By proactively addressing these challenges, BlitzScore simplifies adoption—allowing lenders to modernise without technical friction.