Merchant onboarding does not end at document collection.

The real operational question comes after that:

Should this merchant go live now, go live with controls, or go to review?

That is where many acquiring workflows slow down.

A merchant may complete KYB, pass core checks, and still enter a review queue because the workflow cannot assign the next step clearly enough. When that happens too often, activation slows, review teams get overloaded, and low-friction merchants wait longer than they should.

What should trigger merchant review before go-live?

Merchant review before go-live should be triggered only when the workflow cannot assign a reliable activation decision through verification, classification, and routing logic alone. In practice, review should be reserved for merchants with material inconsistency, elevated risk sensitivity, unclear classification, or control-sensitive activation needs.

That matters because not every imperfect merchant case needs manual review.

Some need clarification. Some need additional controls. Some are ready to go live. If all of them enter the same queue, review becomes a bottleneck instead of a control layer.

Why merchant onboarding alone is not enough

Merchant onboarding helps collect and verify inputs.

It does not automatically decide:

whether activation should happen immediately

whether controls should apply at launch

whether the merchant needs a different review path

whether classification is strong enough for go-live

Cases where the workflow cannot confidently determine merchant category, MCC alignment, control design, or go-live path. That is also why AI-Driven Merchant Verification & MCC Mapping matters before activation.

4. Control-sensitive activation decisions

Merchants that may require tighter limits, enhanced monitoring, or closer scrutiny from day one.

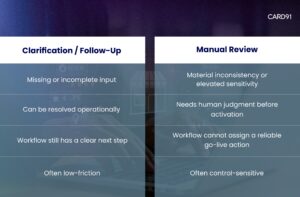

Merchant Clarification vs Merchant Review

Many queues become overloaded because cases that need clarification are sent to review instead.

What better acquiring teams do differently

Stronger teams usually do five things better:

connect onboarding to go-live action

separate merchant validity from merchant readiness

CARD91’s acquiring stack is built around this exact shift.

Across merchant onboarding, verification, classification, MCC mapping, and lifecycle workflows, the goal is not only to onboard merchants faster, but to help banks decide more clearly before activation. That means using merchant signals to support better routing, better control design, and better go-live decisions.

That is why reducing merchant review before go-live is not about lowering scrutiny.

It is about applying scrutiny more precisely.

Key takeaways

Merchant review before go-live should be triggered only for exception cases.

Not every imperfect merchant case belongs in manual review.

Material inconsistency, elevated risk sensitivity, classification ambiguity, and control-sensitive activation needs are the strongest review triggers.

Clarification and review should not be treated as the same path.

Better go-live frameworks reduce delay without weakening control.

Final thought

Merchant review is not the problem.

Poor review design is.

The goal is not to send fewer merchants into control.

The goal is to make sure only the right merchants reach merchant review before go-live: Book a demo with CARD91

FAQs

Q: What should trigger merchant review before go-live? A: Merchant review before go-live should be triggered when the workflow cannot assign a reliable activation decision because of material inconsistency, elevated risk sensitivity, classification ambiguity, or control-sensitive activation needs.

Q: Should incomplete merchant information always trigger review? A: No. If the issue can be resolved through clarification or follow-up, it may not require full manual review.

Q: What is the difference between merchant clarification and merchant review? A: Clarification is used when missing or incomplete inputs can be resolved operationally. Review is used when human judgment is needed before activation.

Q: Why do merchant review queues become bottlenecks? A: They become bottlenecks when too many low-friction or poorly segmented merchant cases are sent to manual review by default.

Q: How can banks reduce merchant review delays before go-live? A: Banks can reduce delays by connecting onboarding outputs to go-live decisions, improving classification, making review selective, and aligning controls to merchant context.