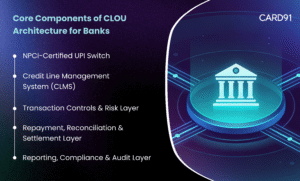

A production-ready CLOU architecture consists of five tightly integrated layers.

The UPI switch is the entry and exit point for all CLOU transactions.

For CLOU, the UPI switch must support:

Without a certified, production-grade UPI switch, CLOU cannot scale safely.

The CLMS is the heart of CLOU architecture.

It acts as the system of record and control for all credit line activity, managing:

During every CLOU transaction, the CLMS:

Without a CLMS, banks lose fine-grained control over credit exposure.

In issuer-grade deployments, this central role of the CLMS reflects why banks need a dedicated Credit Line Management System for Credit Line on UPI, rather than relying on loan or card platforms.

CLOU requires pre-authorisation risk enforcement, not post-facto checks.

This layer applies:

Unlike card systems, CLOU controls operate at the account and scheme level, allowing banks to tailor risk logic precisely.

CLOU repayments are UPI-native, flowing into a unique UPI handle per credit line.

This layer handles:

A tightly integrated reconciliation layer is critical to avoid:

Because these controls must execute before authorisation, banks design this layer around real-time risk governance for Credit Line on UPI, not post-transaction review mechanisms.

CLOU operates under continuous regulatory scrutiny.

This layer supports:

Banks that design reporting as an afterthought often face operational bottlenecks and audit observations later.