Banks often evaluate credit line on UPI and credit cards as complementary products rather than substitutes.

Introduction: CLOU Is Not a Replacement for Cards—It’s a Different Credit Model

As Credit Line on UPI (CLOU) gains momentum, banks are increasingly asked a strategic question:

Is CLOU meant to replace credit cards?

The short answer is no.

CLOU and credit cards are fundamentally different credit instruments, built on different rails, with different risk models, customer behaviours, and operating economics. Treating them as substitutes leads to poor product decisions and misaligned expectations.

This article explains how banks should compare Credit Line on UPI and credit cards, and how both fit into a modern issuer’s credit portfolio.

What Is Credit Line on UPI?

Credit Line on UPI allows banks to offer pre-sanctioned, account-based credit lines that customers can access directly via UPI apps using a unique UPI handle.

Key characteristics:

Account-based digital credit

UPI-native transactions

Real-time utilisation and repayment

Dynamic credit limits

Continuous lifecycle governance via a CLMS

CLOU behaves closer to digital lending infrastructure than to traditional card products.

What Are Credit Cards?

Credit cards are card-based revolving credit products operating on card networks and governed by card billing cycles.

Key characteristics:

Card number and BIN-based identification

Cyclical billing and settlement

Network-defined acceptance and chargeback rules

Mature merchant ecosystem and rewards programs

Cards are optimised for high-value spends, cross-border usage, and long-tenure customer relationships.

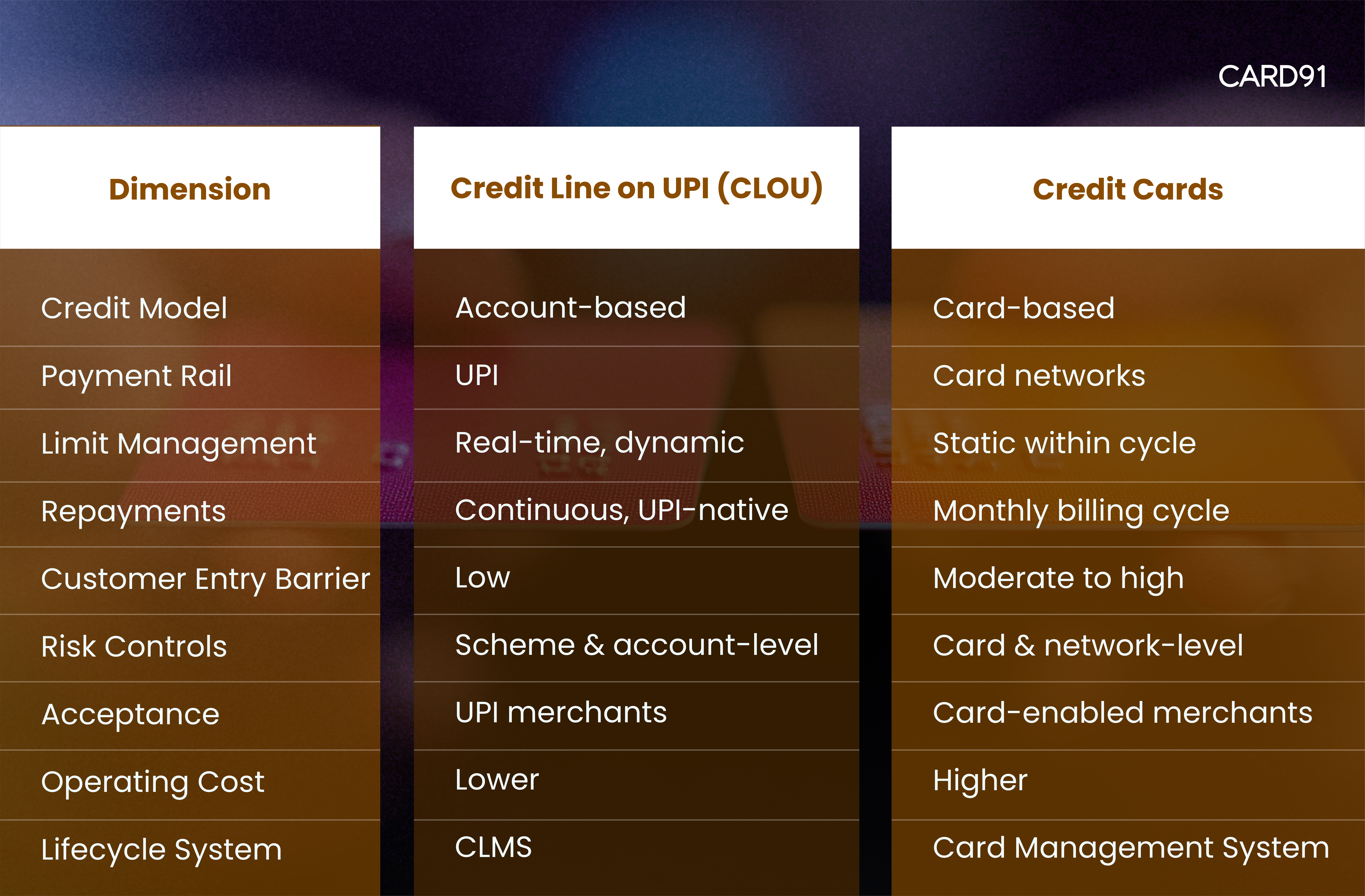

CLOU vs Credit Cards: Issuer-Level Comparison

These differences are reflected in issuer-grade CLOU architecture, where lifecycle management and authorisation controls operate separately from card systems.

CLOU gives issuers more direct control, while cards rely more heavily on network governance.

Customer Behaviour & Use Cases

CLOU Is Best Suited For:

Everyday merchant payments

New-to-credit and thin-file customers

Short-tenure, high-frequency usage

Domestic digital payments

Credit Cards Are Best Suited For:

High-value discretionary spending

Travel, e-commerce, and cross-border usage

Long-term revolving balances

Premium rewards and loyalty programs

These behaviours are complementary, not competitive.

Cost Structure & Portfolio Economics

From a bank’s perspective:

CLOU typically has lower issuance and servicing costs

Credit cards involve higher network, fraud, and chargeback costs

CLOU enables tighter credit-risk control with lower leakage

Cards deliver higher interchange and long-term customer value

A balanced portfolio uses both instruments to optimise risk-adjusted returns.

Strategic Positioning: How Banks Should Use CLOU and Cards Together

Forward-looking banks increasingly follow a dual-rail strategy:

Use CLOU for:

Entry-level digital credit

UPI-centric customer journeys

Fast experimentation with credit products

Use credit cards for:

Mature customer segments

Premium experiences and rewards

Cross-border and high-value use cases

CLOU often acts as a feeder product, helping banks graduate customers into card portfolios over time.

How CARD91 Supports Both CLOU and Card Issuance

CARD91 enables banks to operate both Credit Line on UPI and card programs through issuer-grade infrastructure.

With CARD91, banks can:

Launch CLOU using a unified CLMS and UPI switch

Maintain issuer-controlled risk and lifecycle management

Operate card issuance and processing in parallel

Design segment-specific credit strategies

Scale both portfolios without operational conflict

This allows banks to expand credit access without cannibalising existing card businesses.

Conclusion: CLOU and Credit Cards Solve Different Problems

Credit Line on UPI is not the future replacement of credit cards—it is the future expansion of digital credit access.

Banks that succeed will:

Stop comparing CLOU and cards as rivals

Design each product for its natural strengths

Use CLOU to widen the funnel

Use cards to deepen relationships

The winners will be issuers that build cohesive credit portfolios, not isolated products.

FAQs: CLOU vs Credit Cards

Is Credit Line on UPI cheaper than credit cards for banks? Yes. CLOU generally has lower operational and servicing costs.

Can CLOU replace credit cards completely? No. Cards remain essential for premium, international, and high-value use cases.

Do banks need separate systems for CLOU and cards? Yes. CLOU requires a CLMS, while cards require a card management system.

Looking to build a balanced CLOU and credit card strategy? See how CARD91 helps banks launch and scale both credit rails with full issuer control. Book a Demo